All Categories

Featured

Table of Contents

These compensations are constructed into the purchase rate, so there are no covert costs in the MYGA agreement. Deferred annuities do not bill fees of any type of kind, or sales costs either. Certain. In the recent setting of reduced rate of interest, some MYGA financiers construct "ladders." That indicates acquiring numerous annuities with staggered terms.

For instance, if you opened MYGAs of 3-, 4-, 5- and 6-year terms, you would have an account growing yearly after three years. At the end of the term, your cash could be taken out or taken into a new annuity-- with good luck, at a higher price. You can also use MYGAs in ladders with fixed-indexed annuities, an approach that looks for to take full advantage of return while also securing principal.

As you contrast and contrast images offered by various insurance provider, consider each of the areas detailed above when making your final choice. Comprehending contract terms in addition to each annuity's benefits and disadvantages will enable you to make the very best decision for your economic circumstance. annuity equity. Assume meticulously concerning the term

Secure Life Annuity

If passion rates have risen, you might want to lock them in for a longer term. During this time, you can get all of your money back.

The firm you acquire your multi-year guaranteed annuity through consents to pay you a fixed passion price on your costs quantity for your chosen period. guaranteed period. You'll obtain passion attributed regularly, and at the end of the term, you either can restore your annuity at an updated rate, leave the money at a fixed account price, choose a settlement alternative, or withdraw your funds

Given that a MYGA offers a fixed rate of interest price that's assured for the contract's term, it can give you with a foreseeable return. With rates that are established by agreement for a certain number of years, MYGAs aren't subject to market fluctuations like various other financial investments.

Life With Guaranteed Minimum Annuity

Minimal liquidity. Annuities generally have charges for early withdrawal or abandonment, which can limit your capability to access your money without charges. Reduced returns than other investments. MYGAs might have lower returns than stocks or shared funds, which could have higher returns over the long-term. Charges and expenses. Annuities generally have surrender costs and administrative prices.

MVA is an adjustmenteither favorable or negativeto the accumulated worth if you make a partial abandonment over the complimentary amount or fully surrender your agreement during the surrender cost period. Rising cost of living danger. Due to the fact that MYGAs use a set price of return, they may not keep speed with rising cost of living in time. Not guaranteed by FDIC.

How Much Is An Annuity Worth

It's important to vet the stamina and security of the company you select. Check out records from A.M. Ideal, Fitch, Moody's or Criterion & Poor's. MYGA prices can transform usually based on the economic situation, yet they're typically more than what you would certainly gain on a savings account. The 4 types of annuities: Which is right for you? Need a refresher on the 4 basic kinds of annuities? Discover more how annuities can ensure an earnings in retired life that you can not outlast.

If your MYGA has market value change stipulation and you make a withdrawal prior to the term mores than, the business can change the MYGA's surrender worth based on modifications in rate of interest. If prices have actually increased given that you acquired the annuity, your surrender value may reduce to make up the greater rates of interest setting.

Annuities with an ROP arrangement commonly have lower guaranteed rate of interest rates to balance out the business's potential threat of having to return the costs. Not all MYGAs have an MVA or an ROP. Terms depend on the business and the contract. At the end of the MYGA period you have actually selected, you have 3 choices: If having a guaranteed interest price for an established number of years still lines up with your economic approach, you simply can restore for one more MYGA term, either the exact same or a different one (if offered).

Standard Life Annuity

With some MYGAs, if you're not exactly sure what to do with the money at the term's end, you do not need to do anything. The gathered worth of your MYGA will relocate right into a dealt with account with a sustainable one-year rates of interest established by the business. You can leave it there till you choose your next step.

While both deal ensured rates of return, MYGAs usually use a higher rate of interest price than CDs - annuity plans in usa. MYGAs grow tax obligation deferred while CDs are exhausted as revenue yearly.

This lowers the potential for CDs to benefit from long-lasting compound interest. Both MYGAs and CDs usually have very early withdrawal charges that may impact temporary liquidity. With MYGAs, surrender charges might apply, depending on the type of MYGA you choose. So, you may not only weary, but also principalthe cash you originally added to the MYGA.

Types Of Annuities And How They Work

This means you might weary yet not the principal quantity added to the CD.Their conventional nature often appeals much more to people who are approaching or currently in retired life. However they might not be appropriate for every person. A might be best for you if you wish to: Benefit from an ensured rate and secure it in for a period of time.

Take advantage of tax-deferred earnings development (benefits and risks of annuities). Have the choice to pick a negotiation option for a guaranteed stream of income that can last as long as you live. Similar to any kind of savings lorry, it is very important to carefully evaluate the terms of the product and seek advice from to identify if it's a sensible option for attaining your private demands and goals

Interest Rate On Annuity

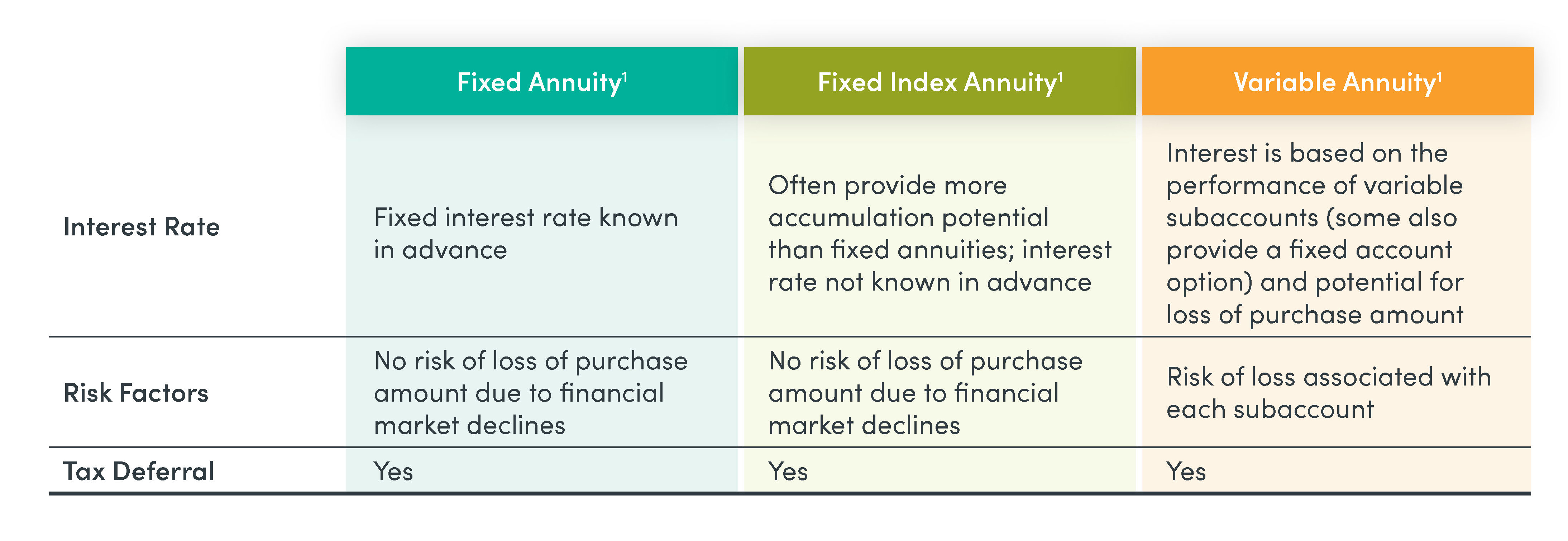

1All warranties consisting of the death benefit repayments depend on the cases paying capability of the issuing business and do not use to the investment efficiency of the hidden funds in the variable annuity. Possessions in the underlying funds are subject to market dangers and may rise and fall in worth. Variable annuities and their hidden variable investment choices are offered by prospectus only.

This and various other details are contained in the syllabus or recap syllabus, if offered, which might be gotten from your financial investment professional. Please review it before you spend or send out cash. 2 Scores go through alter and do not apply to the hidden investment options of variable items. 3 Current tax legislation is subject to interpretation and legal modification.

The Standard Annuity Rates

People are urged to seek certain advice from their individual tax or lawful advise. By providing this web content, The Guardian Life Insurance Company of America, The Guardian Insurance Coverage & Annuity Company, Inc .

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments Key Insights on Fixed Income Annuity Vs Variable Annuity Defining the Right Financial Strategy Benefits of Fixed Interest Annuity Vs Variable Inv

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future Defining the Right Financial Strategy Benefits of Choosing the Right Financial Plan Why Choosing the Right

Understanding Fixed Indexed Annuity Vs Market-variable Annuity A Closer Look at Variable Annuity Vs Fixed Annuity Breaking Down the Basics of Investment Plans Benefits of Fixed Income Annuity Vs Varia

More

Latest Posts